So I decided to take a quick look at this and found something interesting. People used to use yield spreads as a proxy for bank profit margins. The ones that you would hear about were the 10 year treasury rates versus 2 year rates or Fed Funds rate or some such thing. When that was wide, bank margins were wide and vice versa.

Anyway, the following are just some thoughts. Don't read this if you want answers. I have no idea, frankly, if the U.S. will follow Japan; I have no idea how long interest rates will stay low. I do actually have a hunch that it will stay low for a lot longer than most people think, though, but that doesn't mean I think we are in for a Japan scenario.

And keep in mind, I am not predicting a Japan scenario here. It is my personal, primary risk scenario, not the base-case scenario. My base-case scenario, perhaps naively, is that we just muddle along and do OK. Other risk scenarios are of spiking interest rates and hyper-inflation. I tend to lean more towards the deflationary collapse risk side than the hyper-inflation side.

In any case, I don't know which we will see if any. This post will not try to answer that question, nor will this try to figure out if WFC and other banks are good buys here or not. I just wanted to take a closer look at the moving parts, that's all. Think of it as a meditation on NIM, or whatever...

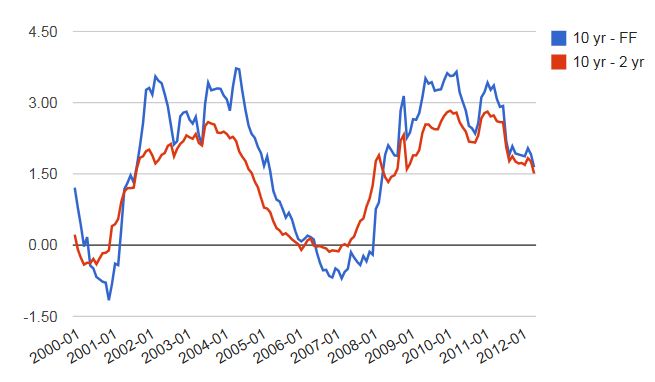

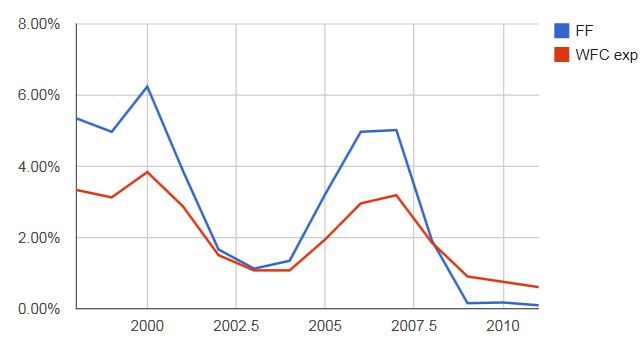

Yield Curve Spread

Anyway, since NIM is my primary concern, naturally, the first thing I should look at is the yield curve spread. Here's a long term and shorter term chart of both yield spreads:

Yield Curve Spread

(10 yr versus FF rate and 10 yr versus 2 yr, annual data)

This is the two spreads going back to 1985. Any further back may not be as important due to Reg Q (regulated interest rates) etc. This chart goes to the end of 2011. So despite very low long term rates, as of the end of 2011, spreads were still at the *upper* end of the range since the 1980s. Of course, that's due to the very low short term interest rates. As of the end of 2011, you can safely say that the low interest rates on the short end of the curve has been very beneficial to banks.

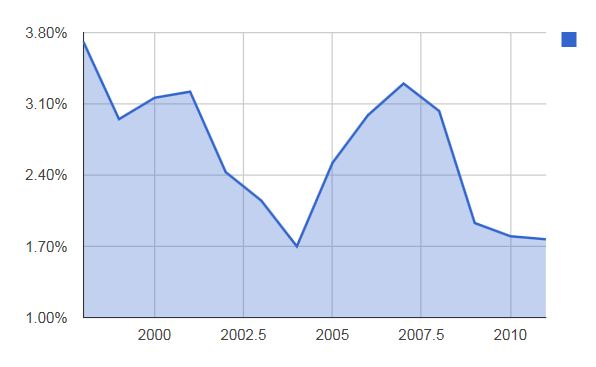

Here's the same data on a monthly basis since 2000 and through the end of May:

Yield Curve Spread

(10 yr versus FF rate and 10 yr versus 2 yr, monthly data)

So even including the recent plunge in long term rates, the spread is still just about in the middle of the range; the spread is not abnormally low at all. 1.8% is the end of May figure (actually, average for the month of May) for the 10 year treasury rate, and as of now that's 1.62%.

So far, even though long term interest rates have come down to abnormally low levels, thanks to the super-low short end, spreads are still within 'normal' range.

That's good news; despite declining long term rates, the yield curve is still positively sloping enough to be 'normal'.

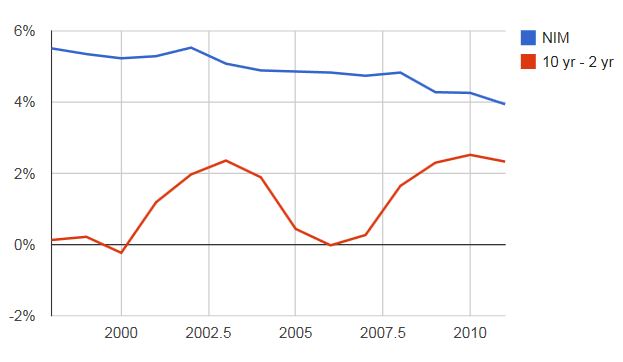

Yield Curve Spread and NIM

So how does the above compare to bank NIMs? Here is some annual data for Wells Fargo (WFC) going back to 1998 or so. I plotted the NIM against the 10-2 Treasury yield spread.

Wells Fargo NIM vs. 10-2 spread

The bad news is that NIM has been trending down over time regardless of the spread.

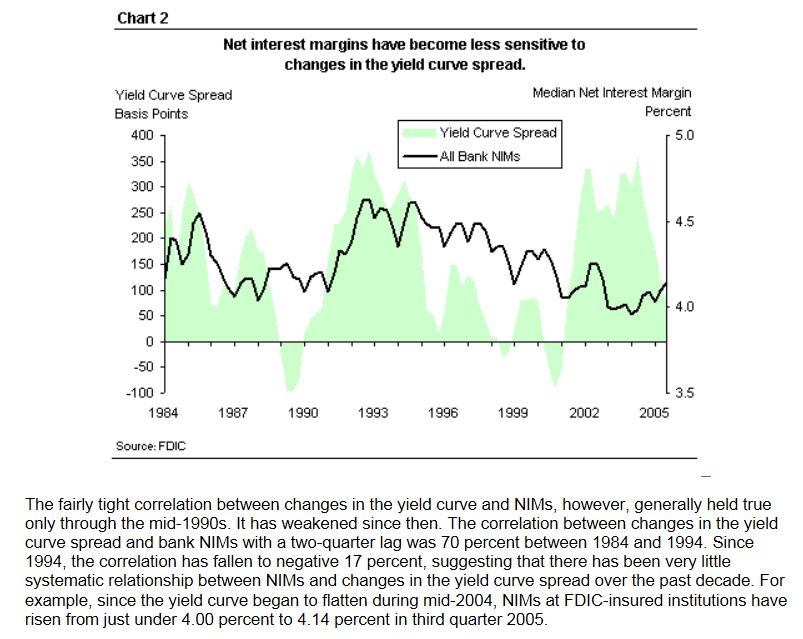

Here is the NIM for all banks from a FED website. It's the quarterly NIM for all banks. This too, shows a steadily declining trend in NIM regardless of the yield curve.

This is from an FDIC study on net interest margins and yield curve spread back in 2006. They do note the decline in correlation between bank NIMs and the yield curve:

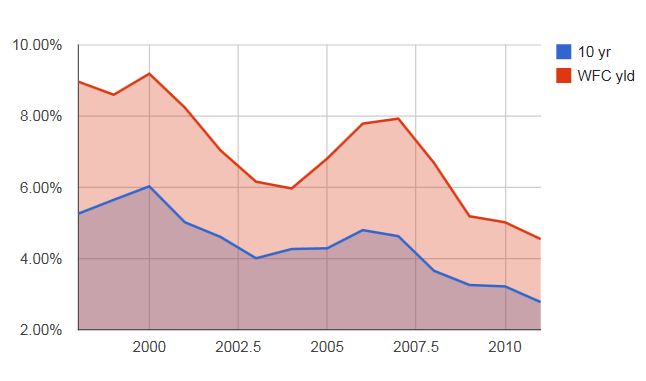

Just for reference, here's the 10-year yield:

10-Year Treasury Yield (annual averages)

So What Does That Mean?

Since the yield curve spread isn't helping us see what's going on with NIM, let's take a look at the actual components.

First, we'll look at the asset side of the balance sheet.

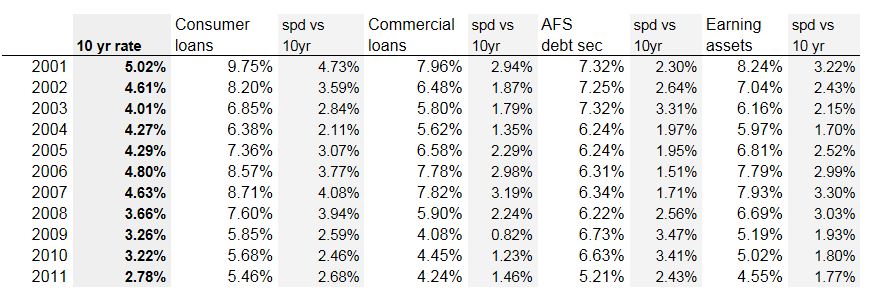

Yield on Interest Earning Assets at WFC versus 10-year Treasury Yield

WFC Funding Cost versus FF Rate

So the yield on earning assets declined 4.4% while funding cost only declined 2.73% for a spread compression of 1.67%. There is our 1.6% NIM compression from 5.5% to 4% or so (well, that's kind of obvious in a declining interest rate environment; no charts needed to tell us that!).

It seems like banks are not correlated at all to the yield curve spread, but are now just correlated to long term interest rates. That can't be good news in this environment.

But let's take a close look at the asset side to see how much of the NIM compression or decline in yield is due to a lower treasury rate and how much due to tighter loan spreads.

Below is the chart that shows the difference between the yield on earning assets spread versus the 10-year treasury rate:

WFC Yield on Earning Assets minus 10-year Treasury Rate

WFC yield on earning assets went from 8.97% in 1998 to 4.55% in 2011, a decline of 4.42%. The ten year treasury rate went from 5.25% to 2.78% during that time (annual averages) for a decline of 2.48%, so 56% of the decline in yield is due to lower interest rates in general. The rest comes from a decline in the above spread.

Is this due to change in mix or declining loan spreads? As a quick proxy I just grabbed some data on rates for conventional mortgages and Moody's Baa industrial bond spreads.

Spread Versus 10-year Treasuries: Conventional Mortgages and Baa Industrial

The other explanation obviously has to be asset mix. In the above chart showing the difference between yield on earning assets and treasuries, it's interesting that the last dip occured in 2002-2003, which were weak years in the economy. Banks tend to invest in treasuries and other securities and make less loans in a weak economic environments which may be the case now.

Asset Mix

So if the decline in yield on earning assets spread (versus 10-year treasuries) is not due to declining loan spreads, it can only be asset mix.

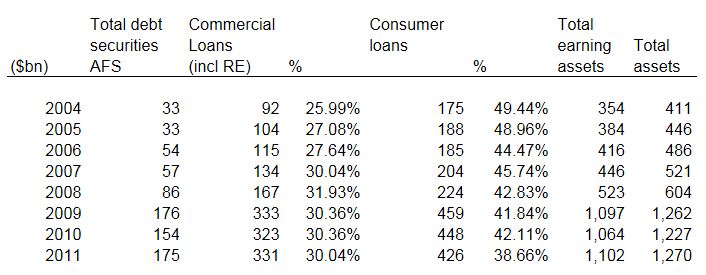

Here's the asset mix for WFC since 2004:

Well's Fargo's Interest Earning Assets

What I suspected was that during bad economic times, banks would make less loans and invest more in low yielding fixed income securities (like JPM's controversial $370 billion bond portfolio). WFC management has also said during conference calls that some of the recent NIM declines were due to deposit growth outpacing their ability to make good loans; cash piles up in treasuries and other low-yielding securities decreasing yields on earning assets.

The above table does indeed show an increase in total debt securities available for sale over the past few years. The only problem with that is that it looks like the yield on available for sale debt securities is actually higher than the total yield on all earning assets (5.21% versus 4.55% in 2011 and 6.63% versus 5.02% in 2010). This may have something to do with a legacy portfolio from the Wachovia acquisition.

However, it is notable that consumer loans have declined from 49.44% to 38.66% from 2004 to 2011. That's a pretty large drop, and commercial loans went up from 26% to 30%. It looks like commercial loan yields are much lower than consumer loan yields so that would certainly be a factor in declining NIM.

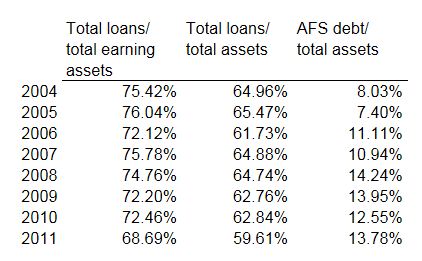

I think typically the earnings asset yield is linked to the percentage of total loans to total earning assets (or total assets) as loans tend to have higher yields than securities (that banks typically buy with deposits not lent out).

Below are the figures for WFC:

Breakdown of Total Loans and AFS Debv to Total Assets

To get more color on how all of this impacts yield and NIM, I just jotted down yields on the major earning asset categories at WFC, and here it is:

Yield on Earning Assets by Major Categories (WFC)

I just put the 10-year treasury rate and spread in there for reference; of course we don't know the terms of the loans and they are most likely not 10 years, so this isn't apples to apples.

You will see that consumer loans usually have much higher spreads than the other categories. So the declining percentage of assets going to consumer loans is a big factor (other than declining overall interest rates, which accounted for about half of the decline in yields since 1998), which makes intuitive sense.

And contrary to the spread chart above where I compared 10-year treasuries to rates on conventional mortgages and Moody's Baa Industrial bond yields, there does appear to be spread compression in WFC's book. But this, of course, may be due to mix; they may be more selective in making loans and making only high quality loans (and therefore earning less yield). This is consistent with what is understood to be going on in the industry. WFC has said in conference calls that they are not seeing spread compression due to competition between lenders.

ROAA and ROAE

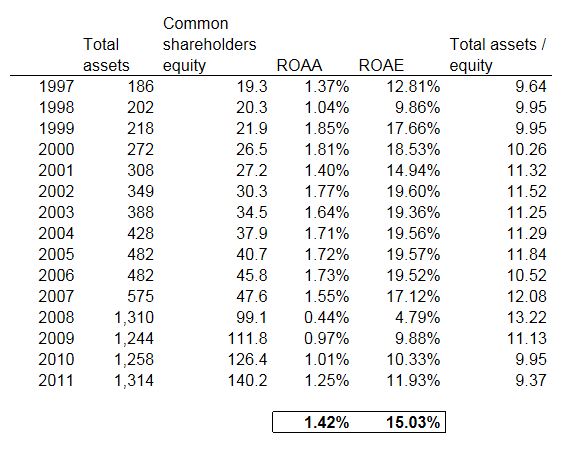

So how does all of this affect return on assets and return on equity? Just out of curiosity I just jotted down the return on average assets (ROAA) and return on average equity (ROAE) of WFC since 1997.

Return on Average Assets and Equity of Wells Fargo

($billions except % and leverage (x))

I also added the ratio of total assets to shareholders equity so we can see how 'leverage' impacts ROE over time. The argument is that banks can't be as levered as they used to be so looking at this would give us an idea on the impact of such changes in leverage going forward.

Anyway, it looks like despite low interest rates, WFC was able to earn an ROA of 1.25% versus an average since 1997 of 1.42%. In good times WFC seems to earn ROA of 1.7-1.8% area, and this may be possible again in a stronger economy. They are earning over 1.0% in this horrible environment so that's encouraging.

ROE at around 12% is slightly below the 15% average since 1997 and that is due to both a slight decrease in leverage and lower ROA. But again, this is in a very weak environment with housing still flat on it's back.

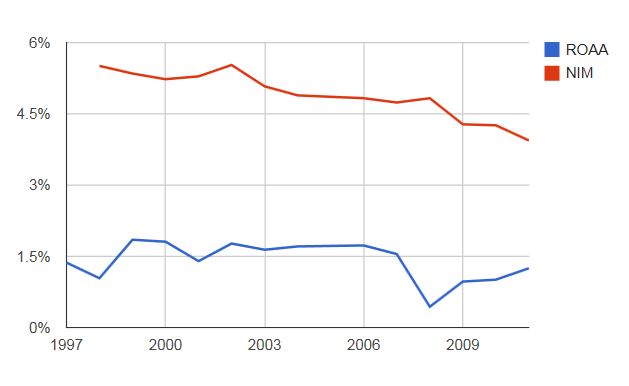

ROAA versus NIM

So naturally, we would want to see ROAA versus NIM to see what declining NIMs has done to it over time. It looks like WFC was able to maintain decent ROAA despite decreasing interest rates and NIM.

NIM is not a risk-adjusted figure, so that sort of makes sense. When you make risky loans, NIM goes up, but so does loan losses. If you manage the portfolio well, NIM can go down but profits can stay stable if you make better loans and write off less. This is what I guess is happening at WFC (and other banks). Non-interest income from fees also helps mitigate the decline in NIMs.

If the economy starts to pick up and housing starts to move (as many people are starting to expect), then I wouldn't be surprised if WFC starts to earn over 1.5% on assets despite the interest rate environment (and interest rates may go up if housing recovers too, but it may not since global interest rates may be under pressure due to the deleveraging that still needs to take place around the world).

Conclusion

It's interesting to see that despite dramatically lower long term interest rates, the yield curve is still well within the historical range. If rates stay down here, banks can still do OK as long as they can make decent loans. There is nothing in the term structure of interest rates now that says banks can't do well.

However, if interest rates keep going down, then this will obviously be a problem. This would indicate a weak economy for a longer time so loans probably won't increase too much and there may not be much opportunity to make higher yielding loans; increasing credit quality of portfolio may lead to lower and lower yields as has been the case in the past few years.

Obviously the economy would need to pick up for WFC to see loan growth and expanding interest rate margins.

It is interesting to see that NIM continued to decline even in the very strong economy of 2005-2007. At the time, I think the argument was that irrational, non-banks and securitization markets caused loan rates to go down to unreasonable levels, but that's not really proven in the chart comparing earning asset yields to Treasuries; the spread was fat in the good years.

In any case, WFC has shown it's ability to earn 1.7%-1.8% return on asset despite declining NIM and long term interest rates. If long term rates don't continue to decline too much and housing starts to turn, it would not be a stretch to imagine WFC doing very well.

Anyway, it looks like NIM declines are not necessarily driven by the yield curve but by lower long term interest rates. The yield on earning assets have declined partly due to lower long term interest rates and also due to a declining spread on loans, but this seems to be due to asset mix/loan quality issues rather than declining spreads due to competition between lenders. Much lower portion of the loan portfolio going into consumer loans is a big factor.

So anyway, we are back to what we knew in the first place; WFC is doing pretty good in this awful environment but can do really well if housing/economy really does pick up (and if consumer loan demand goes up). If interest rates stay down here, WFC can actually still do well, just not great.

But if long term interest rates continue to decline and housing doesn't recover, then that will be a problem; WFC may end up having to put more of their deposits into low yielding Treasuries and that would not be so great. That would be like the Japan scenario, even though I would think that WFC management would respond more quickly to such a scenario and not just sit there and hope.

Thank you for sharing your thoughts, as always.

ReplyDeleteFor the sake of discussion, I'm curious what you think would happen if long term rates rose - not because of economic strength, but because the bond vigilantes returned and demanded a higher yield?

Assuming a 5 year duration on a bank's loan book, if rates rose by 2% then the market value of the loans would decline by 10%. If loans/equity = 10 today, then this rise in rates would wipe out all of the bank's equity on a mark-to-market basis. Obviously if rates rose more, then on a mtm basis things are even worse from a balance sheet perspective.

Do you think that this can't happen? Or, do you think that this wouldn't be a big deal?

It would make a fascinating blog post to see how top-notch banks fared in that environment. But, I'm sure the data will be harder to dig up.

Thank you for the excellent blog!

Cheers,

Tom L

Hi, Thanks for the post.

DeleteBanks are pretty hedged out in terms of interest rate exposure so a scenario like you describe would be highly unlikely. Of course, spiking interest rates would cause all sorts of problems to be sure, but not a linear loss like that.

If you dig into the 10K's, banks will usually have some sort of sensitivity analysis somewhere that tells you what happens to the balance sheet with 100 bps, 200 bps shifts in interest rates, yield curve etc.

For WFC, I didn't see a table but there was a description in the risk sectinon (page 78) that said that earnings at risk are less than 1% for moves up and down in interest rates. The declining rate scenario was FF unchanged and 10-year Treasuries averaging below 2.0% yield, and the rate rise scenario is for the FF to go to 3.75% and 10-year to go to 5.10%. If those scenarios happened, the earnings at risk (for next 12 months) would be less than 1%.

That seems implausible, I know. But through swaps and whatnot, banks have matched up their assets/liabilities pretty tightly.

You can go through other bank 10-K's and see all of that.

Of course, the problem is that these are 'static' analyses, so they won't tell you what happens in a crazy, volatile environment like the 70s. They just tell you, with the current portfolio as it is and with swaps and other positions in place, if interest rates moved like this or that, this is what the impact would be.

etc...

Hi kk,

DeleteThanks for the reply. I'm new to banking, so hopefully my questions aren't too basic.

Regarding WFC, on p78 they talk about earnings at risk over the next 12 months - but this seems different to me than their balance sheet risk.

My understanding is that the balance sheet could take a hit on a mark-to-market basis, while earnings are relatively unaffected. This is because loans may be accounted for on a held-to-maturity basis, ie accounted for based on their principle value, not market value. To be concrete, lets assume a 5 year loan maturity, 4% loan yield, and 0% deposit cost. Now lets assume that long term rates jump by 2% tomorrow. The economic value of the loans will decline by about 10%. However, the income statement for the next year will be relatively unaffected. The accounting will still show about a 4% NIM. If this is obvious, I apologize.

I'm trying to understand the duration of WFC's ~$750B loan book. I can't seem to wrap my head around this even after going through their 10-K. The best I can find is Table 13 on p43, but this is limited.

Am I missing something obvious? How would you estimate the duration of WFC's assets? If the banks are indeed hedging the duration of their assets (by using swaps to convert fixed payments to floating) then who is on the other side of the hedge? Someone has to have exposure to long-term interest rates.

Thanks for the discussion.

Cheers,

Tom L

Hi, that's a very good point. The interest rate sensitivities for WFC probably just addresses income statement and not the balance sheet.

DeleteA full analysis won't be as simple as you state either because not all loans are fixed rate; many loans are variable rate. You are also right that bank loans aren't typically marked-to-market but held at par less reserves for losses.

But let's say interest rates move suddenly. There will value lost in value of fixed rate loans (that won't be marked), but there will also be a decline in the fair value of liabilities.

Also, to the extent banks may do asset/liability management to hedge this duration mismatch, the fair value loss won't be as large as it seems. The hedge can be on the loan side or the liability side. If a bank does a pay fix/receive float swap, then they can lock in their funding cost and if that is lower than their loan rate, that cash flow stream is locked in at that point so it would be immune to interest rate fluctuations (but not to changes in the discount rate to put a value on that). If the value of the loans plunge, the value of the 'pay-fixed/receive float' swap would go up.

It is pretty complex for sure.

Anyway, the first thing I would do is (if you are worried about duration mismatch) see how much of the loan book is fixed versus floating rate. Then see the duration of the liabs (long term debt).

I think in the old days there was more discussion about this in the 10K's, but WFC doesn't seem to talk about this much in the recent 10K.

I may be wrong, but I tend to think they are pretty matched these days (after all the problems that have occured in the past 30 years).

If I find something, I'll post it here...

OK, I took a quick look. I may look into the swaps and hedges later if I have time, but for now here is where I would start:

DeleteWFC has $770 billion in loans outstanding. A big rise in rates would cause the fair value of this portfolio to decline.

But first, we can already see that $112 billion of this is loans maturing in less than one year. Also, $147 billion of loans more than a year out is floating rate or adjustable rate.

So combining the two, that's $259 billion. So the interest rate exposure only applies to the other $511 billion.

We also see that WFC has $141 billion in long term debt outstanding. A rise in rates would cause the fair value of this to decline too, so that would be an offset to the loan portfolio decline (banks often issue bonds for asset/liability management purposes).

So right there, netting out this stuff, you have $370 billion in interest rate exposure. I bet the WFC bond maturities are longer than the loan book, so from a duration standpoint it would probably offset more interest rate risk than the amount of bonds outstanding suggests.

This is before any swaps or other hedges.

I did say above that banks are probably matched up duration-wise, but that's probably an overstatement.

To the extent that they don't have to mark to market and they can hold loans at a positive spread, it won't hurt the bank and the thinking is probably that rising rates will also mean higher interest income on new loans being made so that would be an offset.

This has been a very useful discussion for me. Thank you.

DeleteI like the analysis you did to get to the $370M net number.

FWIW, I've been doing some more investigation - and the FFIEC call report for Wells Fargo (Sioux Falls) has some very useful information. The call report breaks out values for securities/loans/leases with maturity over 15 years. Securities with 15+ year maturity are roughly $90B and loans/leases with 15+ yr maturity are roughly $130B. So, I'm getting much more comfortable with the loan durations and rising interest rate exposure.

I still wonder who is on the other side of any interest rate hedges? Hedging interest rates via swaps is a zero sum game, so someone has long-term interest rate exposure. Who can that be besides the banks?

Cheers,

Tom L

EDIT TO LAST POST:

ReplyDelete"It would be interesting to see how top-notch banks fared during the rising rate environment of the 1970s."

Tom L

Hi, this analysis is really a change compared to other blogs.

ReplyDeleteI was surfing couple of months ago, trying to understand how the banks invest their money and didnt quite get the problem with NIM. Could you explain me, how they finance themselves and how do banks invest that money. I suppose that, they collect cds and invest in consumer loans, but why is the spread 10yr - 2yr so important? How and why banks manage to pay for the 1 year deposits more then a 1 year treasury rate, why they don't borrow money from other institutions for lower rate instead?

Also, if the rates go down, why they just don't pass it to the consumers (both commercial and depositors) and keep NIM stable?

If this is too many questions, maybe you could recommend me online article or maybe a textbook so I could read it, because I am thinking about this for a long time, and it frustrates me that I still don't understand it.

Thanks in advance,

Do you have a twitter account?

Thanks for the comment; no, I don't have a Twitter account.

DeleteBanks basically take deposits from customers (checking accounts, savings accounts, CDs etc.) and take those funds to make loans; credit card loans, mortgages, commercial and industrial loans etc.

The 10-2 is important (or was more important in the past) because the 10 year was a proxy for loan rates and the 2 yr was a proxy for funding costs (deposit rates, savings accounts, CDs etc. tend to correlate with the short end of the curve (they also lend/borrow at the Fed Funds rate) and loans (mortgages, for example) tend to correlate with longer term yields.

That's the basic, simple model of how banks operate.

Typically, if long term interest rates go down, it's OK because short term rates go down too; if loan yields go down, funding cost goes down too so it's OK.

Now with short term rates at zero or near zero, further long term rate reductions can't be offset by lower short term rates so any further long term rate reduction just leads to direct NIM reduction and that's no good. That's the problem.

As for how banks work, I don't know of any good books about it.

I find that the best way to learn about an industry is to just order up a bunch of annual reports, 10K's and stuff like that and read as much as you can. If you can bear it, find a small, simple bank and read the 10K from cover to cover. If there are words and concepts you don't understand, just google it and you can find out what it means.

If you do that, try to stay with simple banks; stay away from JPM, C, BAC for example, as they are huge, complex organizations.

WFC is relatively simple, but simple regionals might be better like M&T Bank. Banks in your region might be good to read too.

Anyway, that's the best way to learn about it and the best thing is that all of this stuff is available for free on the internet at company websites and the SEC website...

Fantastic blog. Just wanted to bring the conversation back to the question another poster had earlier that I have never been able to wrap my head around. With all these hedges in order to match the duration (I assume they are also hedging the negative convexity of the mortgage loans?) who is really on the other side. People have told me for years that the banks lay off the risk but where is it really going? At some point, someone has to take that exposure, it doesn't just go away. This has always confused me.

ReplyDeleteI guess at a high level the fixed exposure that is laid off is taken by someone looking for increased duration which should be offsetting another position so if the entire marketplace hedged, they could all net out their exposure? It just seems at some point someone has to take the risk.

Apologies for the long post.

Great post. Too many blogs just put up subjective commentary and not actual facts and figures to back up their opinion. I like what you've done with NIMs and US banks here, and have just added your blog to my RSS reader.

ReplyDeleteKeep it coming!

Hi, nice post. I have been wondering about this topic, so thanks for sharing. I will certainly be subscribing to your blog.

ReplyDelete